Cheap natural gas and increasingly competitive labor costs are bringing factories and jobs back to the U.S. Eight ways to win.

As the only industrialized superpower not decimated by World War II, the United States once made nearly 40% of the planet’s goods. These days, that number has shrunk to 18%. We make American Girl dolls in China, Levi’s jeans in Mexico, and enough movies in Vancouver to nickname it Hollywood North.

After decades of outsourcing, however, the U.S. is quietly enjoying a manufacturing revival, and companies like Apple (ticker: AAPL), Caterpillar (CAT), Ford Motor (F),General Electric (GE), and Whirlpool (WHR) are making more of their goods on American soil again. It isn’t just U.S. companies that are drawn to our cheap energy, weak dollar, and stagnant wages. Samsung Electronics (005930.Korea) plans a $4 billion semiconductor plant in Texas, Airbus SAS is building a factory in Alabama, and Toyota (TM) wants to export minivans made in Indiana to Asia.

The Rust Belt owes its new shine to many factors, including rising wages and industrial-land costs in Asia. But none is bigger than the U.S. energy boom. Thanks to a head start in extracting oil and gas from shales, North America now produces far more natural gas than any other continent. Unlike oil, gas isn’t easily transported across oceans, and a result is some of the world’s cheapest energy within our reach: Natural gas here costs $3.55 per million British thermal units, versus roughly $12 in Europe and $16 in Japan. Cheap energy not only reduces our trade deficit and our addiction to Middle East oil, it also makes our factories more competitive globally — a boon for a country that had gone from exporting American goods to exporting American jobs.

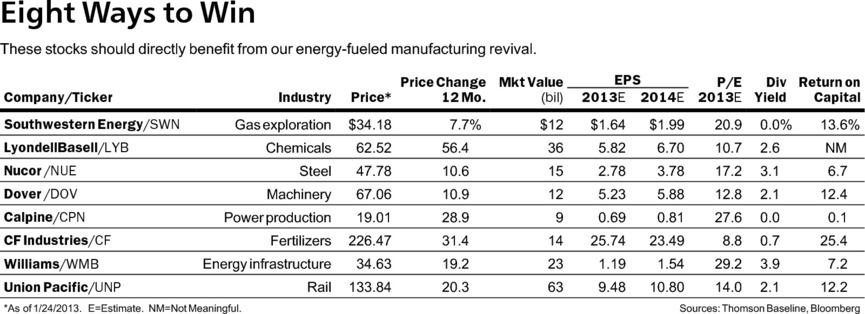

The biggest beneficiaries are energy-guzzling companies like chemical producers and steelmakers, and Barron’s has identified eight stocks that should prosper in our gas-fueled manufacturing upswing. They are Southwestern Energy, LyondellBasell Industries, Nucor, Dover, Calpine, CF Industries, Williams, and Union Pacific. But any glow will also rub off on regional lenders, home builders, and local small businesses. “The U.S. is the Saudi Arabia of natural gas,” declares Nancy Lazar, co-head of the New York research firm International Strategy & Investment. “And Middle America is my favorite emerging market.”

Our energy boom got cracking with fracking, a controversial process in which pressurized fluids are pumped through rock formations, often a mile or more under the ground, to extract oil and gas. Critics condemn fracking, which they contend causes environmental harm, but even they agree that it’s led to an abundance of cheap gas. Over the past six years, U.S. production of petroleum and natural gas has jumped from 15 million barrels of oil-equivalent a day to 20.1 million, a 20-year high. Over the same period, imports have fallen from 14 million barrels a day to below eight million, a 25-year low.

It’s a sign of the times: Graduates from the South Dakota School of Mines & Technology — acceptance rate: 88%; mascot: Grubby the Miner — now command a median starting salary 16% higher than that of Yalies.

By 2020, the U.S. will become the world’s biggest oil producer, says the International Energy Agency. By 2025, North America will be a net energy exporter, predicts ExxonMobil (XOM).

That edge should remain ours for decades. “It isn’t just the huge reserves we have underground,” says Tim Parker, who manages T. Rowe Price’s natural-resource stock portfolios. “No one else has our predictable cocktail of infrastructure already in place, know-how, a relative abundance of water, and a favorable royalty regime that give landowners a stake in the exploration game.” Europe, for instance, is averse to fracking and has little infrastructure; Japan has hardly any shales; and while China has vast reserves, only shales nudging the Yangtze River have enough water for fracking.

Of course, an especially frigid winter could send gas prices soaring, but any such spike should be temporary. Given our expanding reserves and record inventory, commodity strategists expect U.S. natural gas to stay between $3 and $5 per million BTUs for years — well below prices abroad.

CHEAP GAS ISN’T THE ONLY booster in our tank. In the decade since China joined the World Trade Organization in 2001, that nation has become Earth’s low-cost factory. But wages and benefits there are rising 15% to 20% a year, while they’re stagnant here. Despite Beijing’s efforts to hold it down, the yuan has gained 33% against the dollar since 2005. Industrial land averages $10.22 a square foot across China, but rises to $11.15 in the coastal city of Ningbo and $21 in Shenzhen — compared with $1.30 to $4.65 in Tennessee and North Carolina. “Within five years, the total cost of producing many products will be only about 10% to 15% less in Chinese coastal cities than in parts of the U.S. where factories are likely to be built,” says Hal Sirkin, a senior partner at Boston Consulting Group. Add duties and shipping, and the cost gap shrinks further.

Location-scouting manufacturers also are looking beyond mere costs. Moving part of their supply chains closer to the U.S. — still the world’s biggest consumer market — helps companies react faster to changes and also speeds innovation, says Gary Pisano, a Harvard Business School professor. Adds Robert McCutcheon, who heads PricewaterhouseCoopers’ U.S. industrials practice: “You protect not just the intellectual property of your products, but your processes as well.”

Companies, of course, won’t completely shutter overseas factories. U.S. corporate taxes are still high, compared with many other countries’, and there’s a limit to how many jobs will return, given advances in automation and productivity. But BCG’s Sirkin conservatively estimates that 2.5 million to five million manufacturing positions will be added by 2020, which could shave two to three percentage points from our unemployment rate, now near 7.8%. We’ll also expand exports, at the expense of higher-cost developed rivals, such as Germany and Japan. And U.S. ports stand ready and idle, operating at just 54% of capacity, well below 59% in Europe, 67% in Latin America, and 76% in Southeast Asia.

Busier factories would help the entire country. For every dollar spent on manufacturing, another $1.48 is added to the economy, says the National Association of Manufacturers. Another bonus: Manufacturers account for two-thirds of what the private sector spends on research and development.

And we’ve only just begun: Abundant gas and a weak dollar are long-term trends, and U.S. wages should behave until unemployment falls well below 6%, says Jeffrey Korzenik, chief investment strategist at Fifth Third Private Bank. “Offshoring had gone on for decades, but the re-shoring trend is only in year two or three.”

Here are eight stocks that should benefit:

Southwestern Energy (SWN)

Cheap energy is a boon for manufacturers, but a curse for exploration companies, and investors are shunning the producers most exposed to slumping gas prices. With 99% of Southwestern’s production and reserves in natural gas, you’d think the Houston company’s managers would be anxiously sweating over prices near decade lows.

But they aren’t. That’s because Southwestern is a highly efficient, low-cost producer. It works its 926,000 acres in the Fayetteville shale with operational aplomb, using dense wells, some of its own rigs, and vertically integrated services. The company has another 187,000 acres in the Marcellus shale. At $34, its shares trade at a small premium to its gassy peers but still a discount to its net asset value.

Ken Settles, who co-manages the RS Global Natural Resources Fund, expects gas prices to hit $5 to $6 eventually. “But the benefit of focusing on a low-cost producer is that, even with gas prices below sustainable long-term levels, Southwestern’s assets are still profitable and creating value for its owners.”

Southwestern plans to increase 2013 production by 11% to 13%, and analysts see its per-share profit climbing 19% this year. Earnings will grow even more if natural-gas prices rally, but you won’t sweat waiting for that to happen.

Compared with other economically sensitive stocks, Dover is more diverse and more stable. Management has allocated capital shrewdly, making acquisitions, buying back shares, and lifting return on capital to 12.4% — a decade high. Dover has a 2.1% dividend yield, and its 9.7% profit margin trumps the sector’s average. Yet its shares, at $67, trade at 12.8 times 2013 profits, a discount to the market and other machinery stocks.

Calpine (CPN)

Calpine is the largest independent U.S. producer of gas-powered electricity, and runs some of the newest, most efficient plants. Just six years ago, nearly half the nation’s power came from coal. But gas’ share has swiftly risen from a fifth to a third, while coal’s has waned.

The ongoing switch to cleaner natural-gas-generated electricity is one reason whyBarron’s has been bullish about the stock (see “Calpine Gets Ready to Light Up,”July 23, 2012). The company also has unused capacity that puts it in the driver’s seat as utilities replace decades-old coal plants.

At first blush, that advantage seems well reflected in the shares, which, at $19, fetch 27.6 times 2013 profit estimates of 69 cents a share. But that seemingly lofty multiple is below its median over the past five years, and Calpine is generating more than $1 a share in free cash flow and continuing to pay down debt. “When power prices are low, Calpine benefits by taking market share from less-efficient producers,” says MacKenzie Davis, who co-manages the RS Global Natural Resources Fund. “But it also benefits if power prices rise, since margins and cash flow will improve.”